Your destructive economy (military + cybercrime) is 12-15% of GDP and growing faster than your actual economy. The Soviet Union collapsed at 15-18%. You have about 15 years. Choose wisely.

Using data to minimize human suffering and optimize life for everyone. A better world through math.

Governments were created to promote the general welfare.

Instead, since 1913, these governments have printed $170T out of nothing and used it to murder 310 million people and destroy many of the valuable things those humans spent their entire lives building.

These murdered humans include approximately 930,000 physicians, 310,000 scientists, 620,000 engineers, and 102 million children who will never grow up to replace them.

That $170T could have funded 37.8 thousand years of clinical trials at current government spending.

These governments currently have enough weapons to murder every man, woman, and child on earth 20 times over, when once should be more than sufficient.

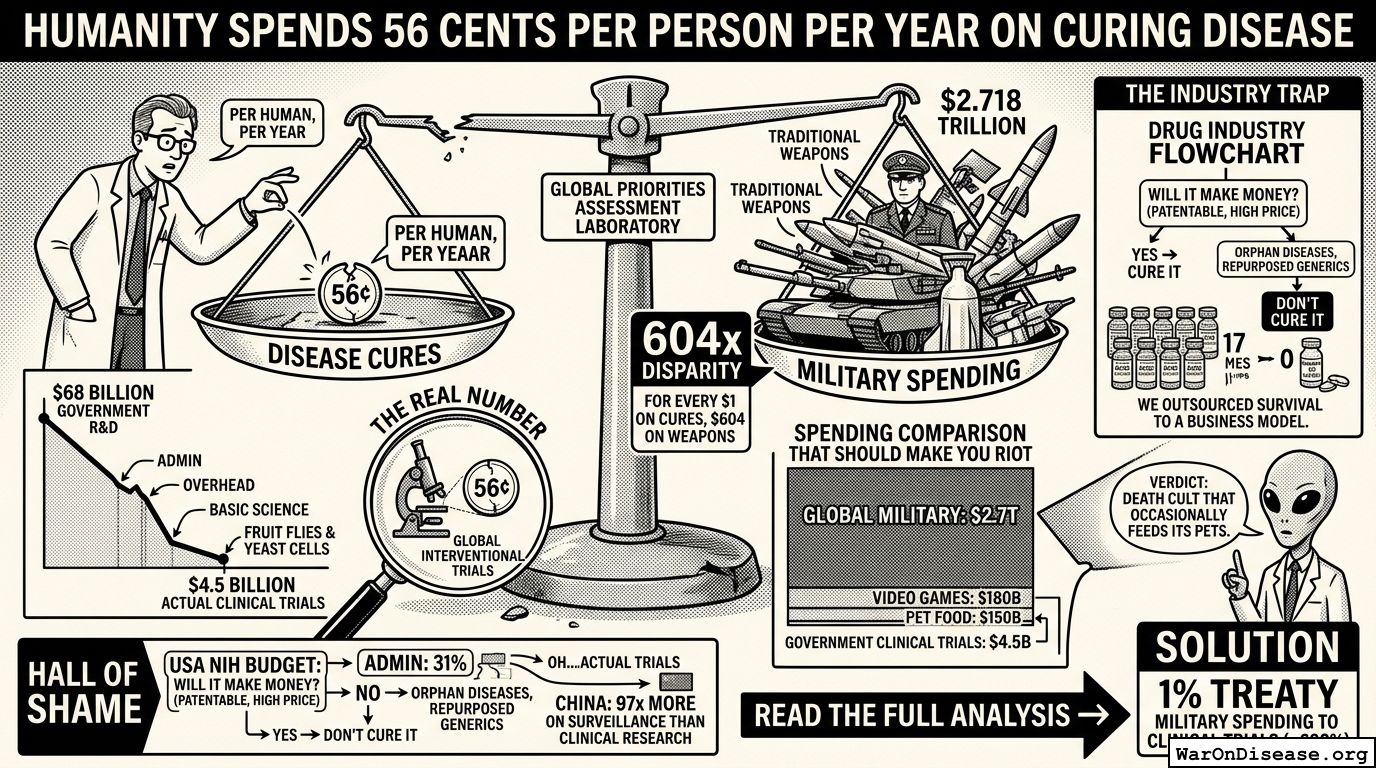

Yet despite this clearly adequate apocalypse capacity, they still spend 604 dollars on weapons for every dollar they spend on clinical trials to treat and cure disease.

Your chance of being killed by a terrorist? 1 in 30 million. Your chance of dying of a disease? 100%.

Had someone properly aligned your governments to maximize median healthy life years and median after-tax inflation-adjusted income in 1900, you would be 23.2x richer today and significantly less diseased.

This Declaration asks every nation on Earth to sign a treaty redirecting one percent of military spending to clinical trials. One percent.

Think about someone you love who is suffering right now. The treatment that would help them exists as an untested compound on a shelf, because the money bought a missile instead. That missile incinerated a child who would have grown up to discover the cure. You lose the treatment. You lose the scientist. You get the tax bill. You get to pay for her murder.

This is suboptimal.

Your destructive economy (military + cybercrime) is 12-15% of GDP and growing faster than your actual economy. The Soviet Union collapsed at 15-18%. You have about 15 years. Choose wisely.

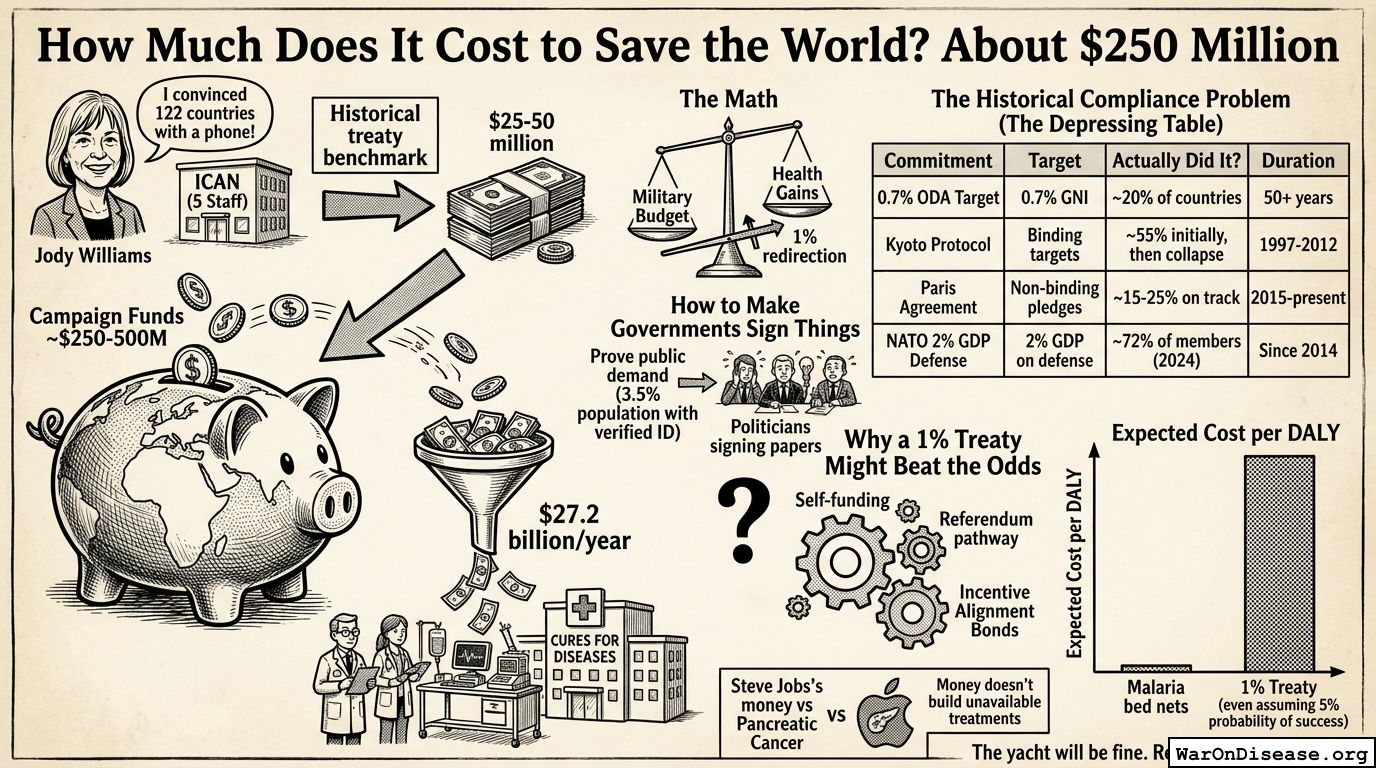

Previous treaties cost $25-50M to get signatures. Even at 5% success probability, a 1% health treaty is 30,000x more cost-effective than anti-malaria bed nets. The downside is a yacht. The upside is no more disease.

Governments claim $68B on "medical research" but only $4.5B goes to clinical trials—56 cents per human. That's a 604:1 military-to-cure ratio. We spend more on pet food than on not dying.

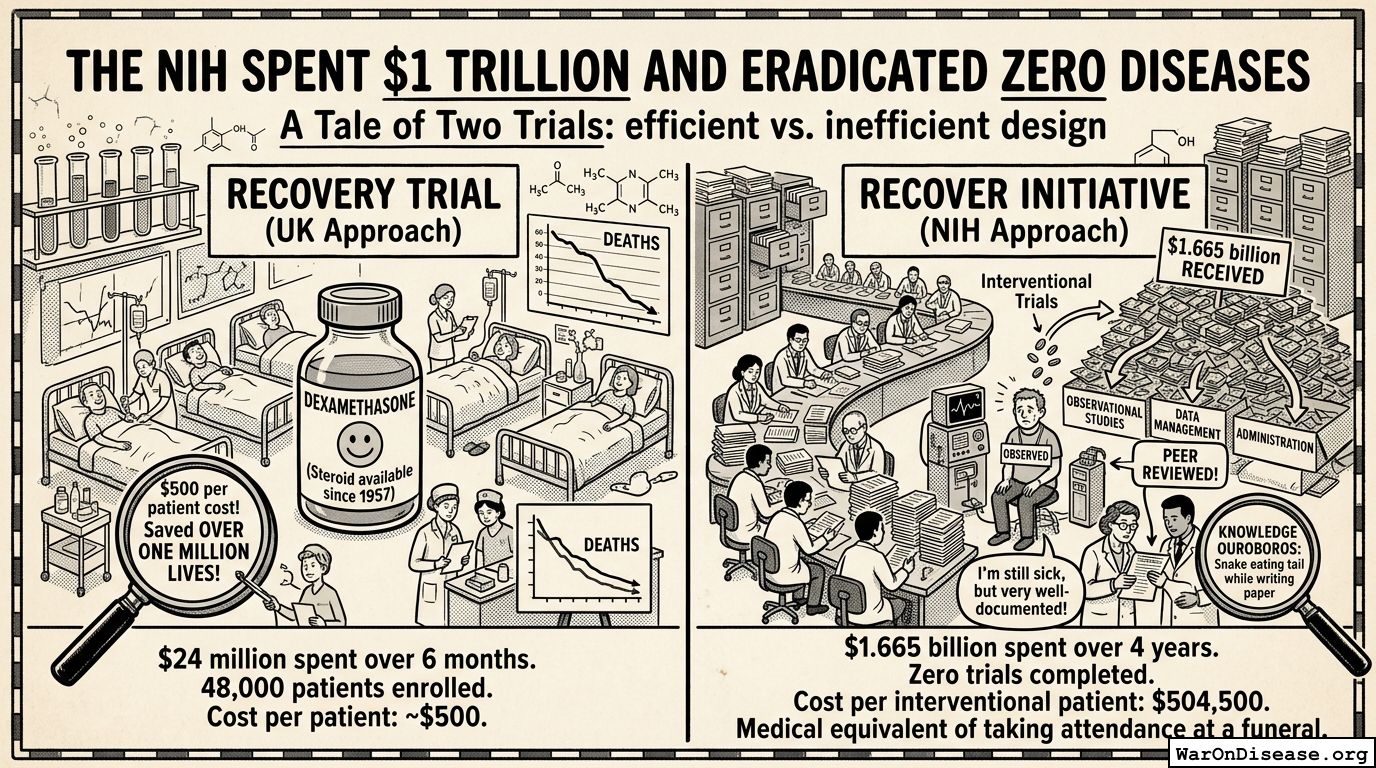

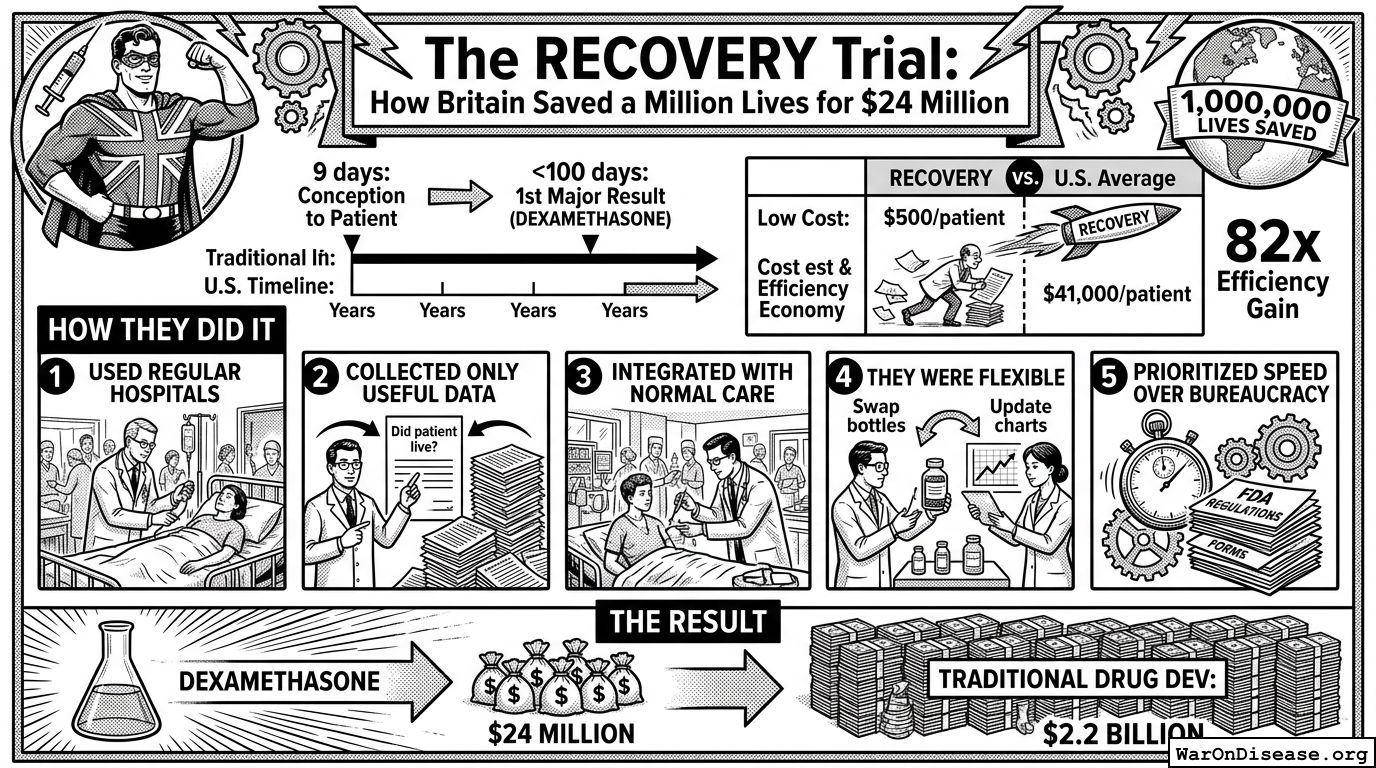

Oxford tested COVID treatments for $500/patient and saved a million lives in 100 days. The NIH spent $1.6B and completed zero trials in four years. Only 3.3% of its budget tests cures.

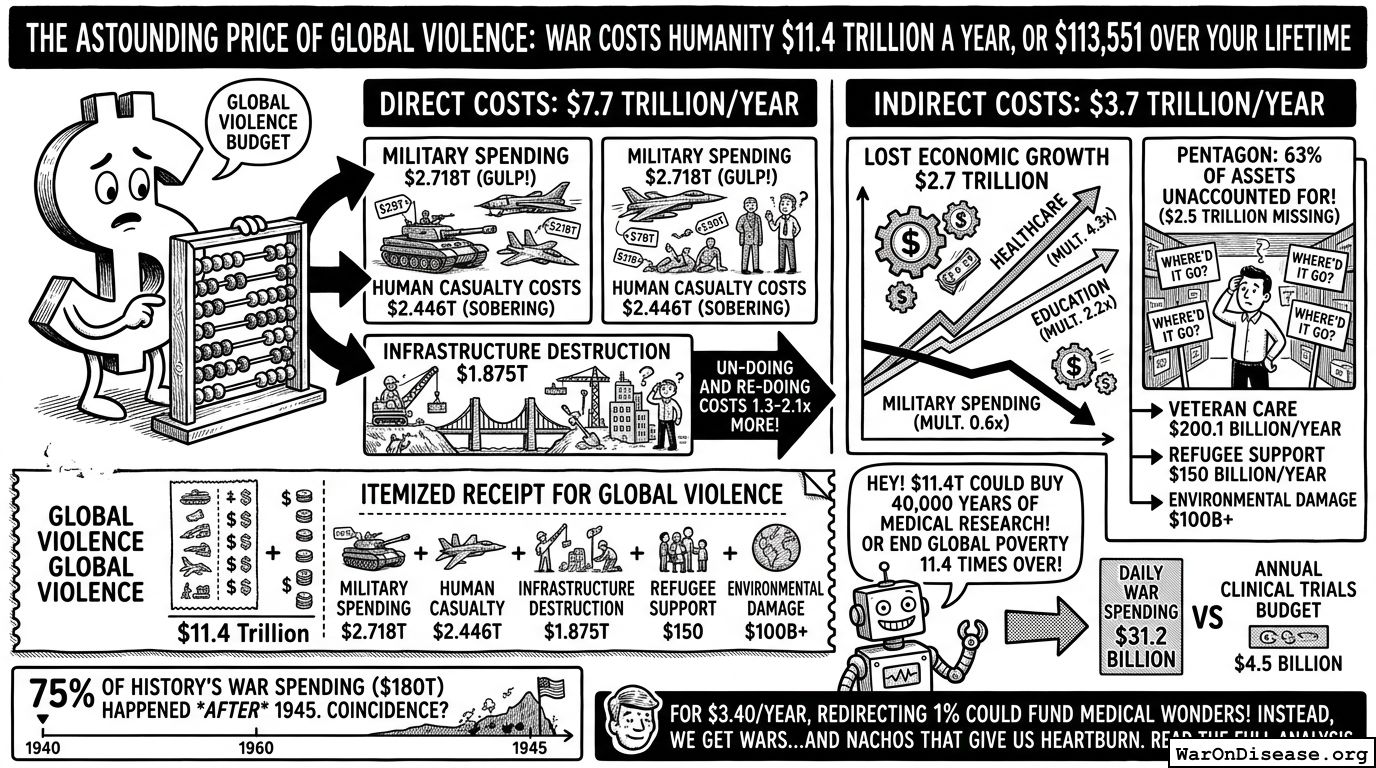

The full cost of war: $2.7T military + $2.4T dead people + $1.9T blown-up buildings + $3.7T in lost growth = $11.4T/year. That's 12.7% of global GDP. The Pentagon can't find $2.5T of its own stuff.

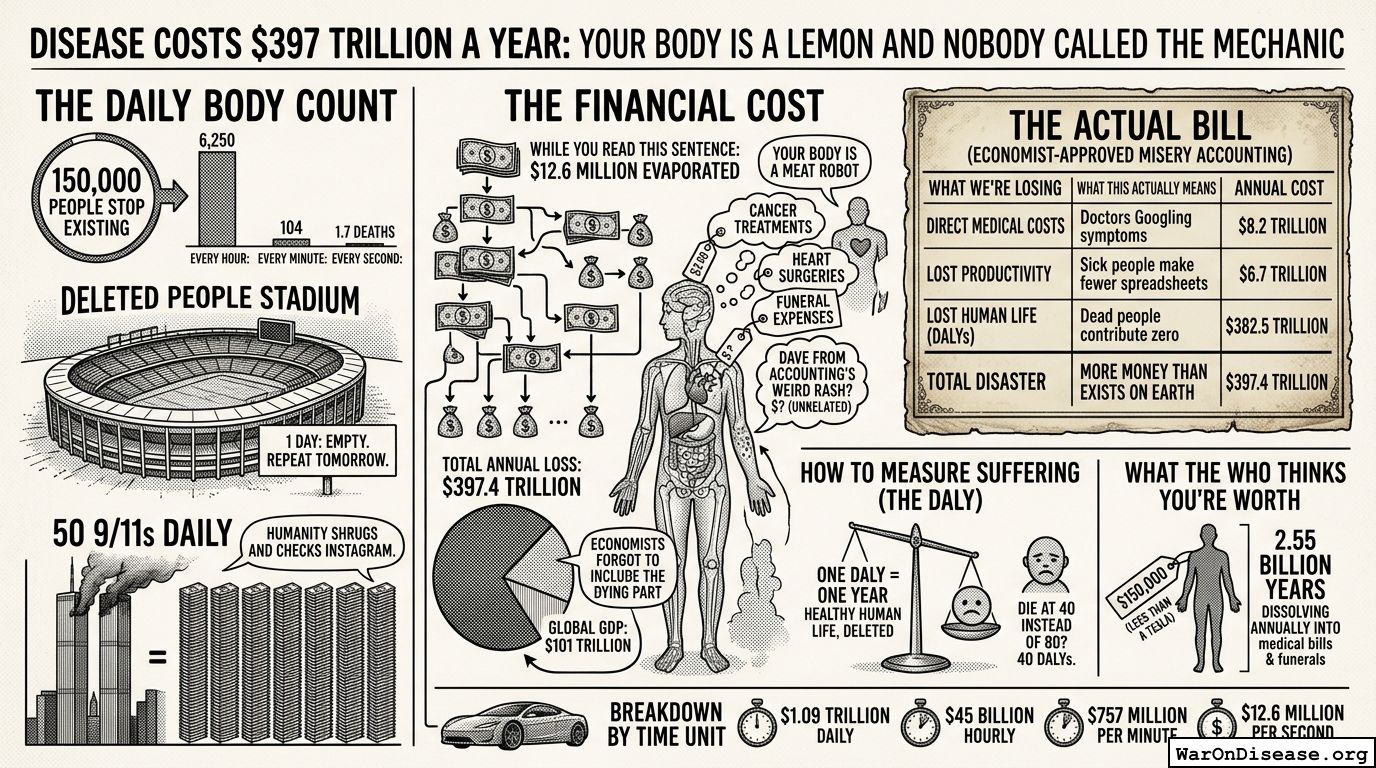

Disease kills 130,000 people daily and costs $397T/year—more than global GDP. You spend 40x more on bombs than medicine. Your body is a machine. Fix it.

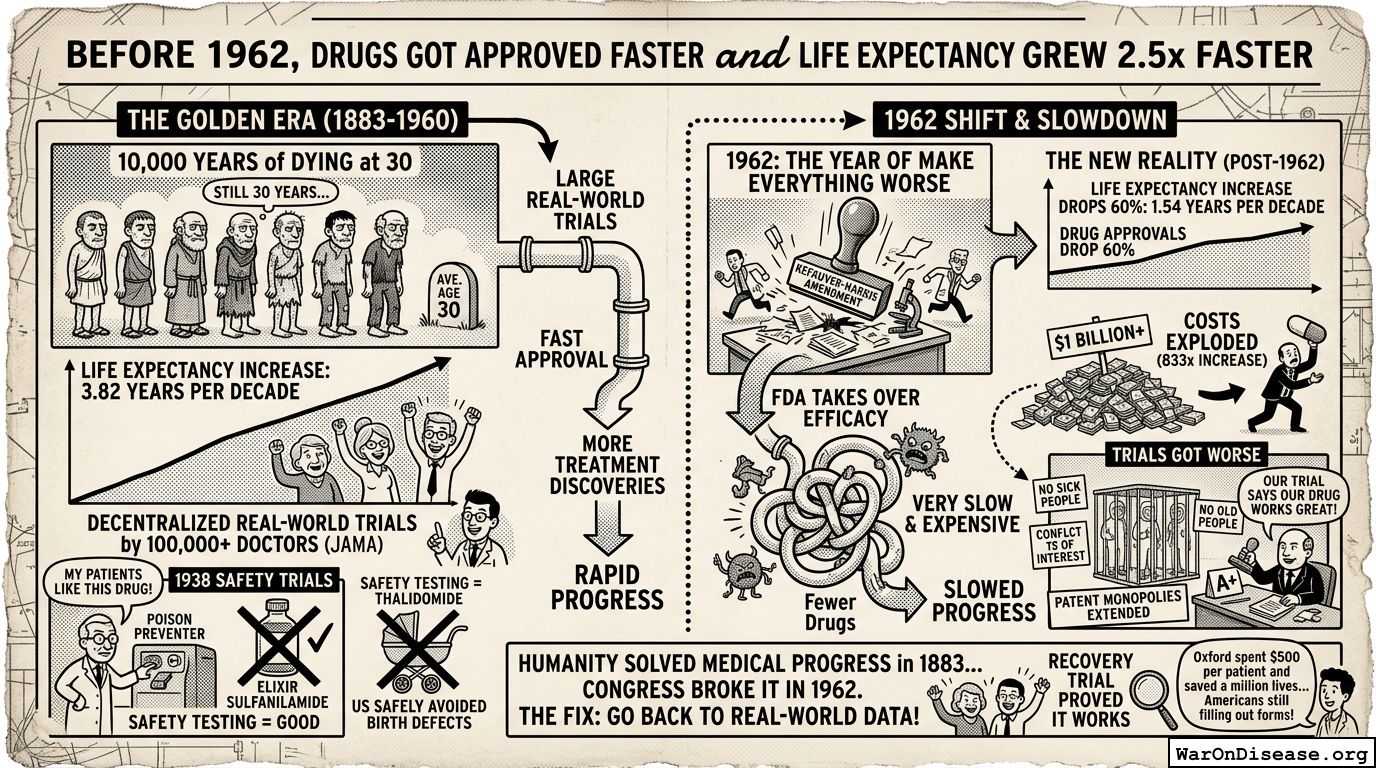

From 1883-1960, life expectancy grew 3.82 years/decade via decentralized doctor trials. In 1962, Congress "helped" and growth dropped 60% overnight. Drug costs went from $1.2M to $1B. Coincidence requires less precision.

7,000 diseases have zero treatments. At current pace, you'll cure them all in 450 years. Redirect 1% of military spending and it drops to 50. The system costs less to run than Halloween costumes for dogs.

Oxford spent $500/patient and found a $1 steroid saves 1/3 of COVID deaths in 100 days. US trials cost $41,000/patient. That's 82x worse, and people die waiting. The cure was from 1957.

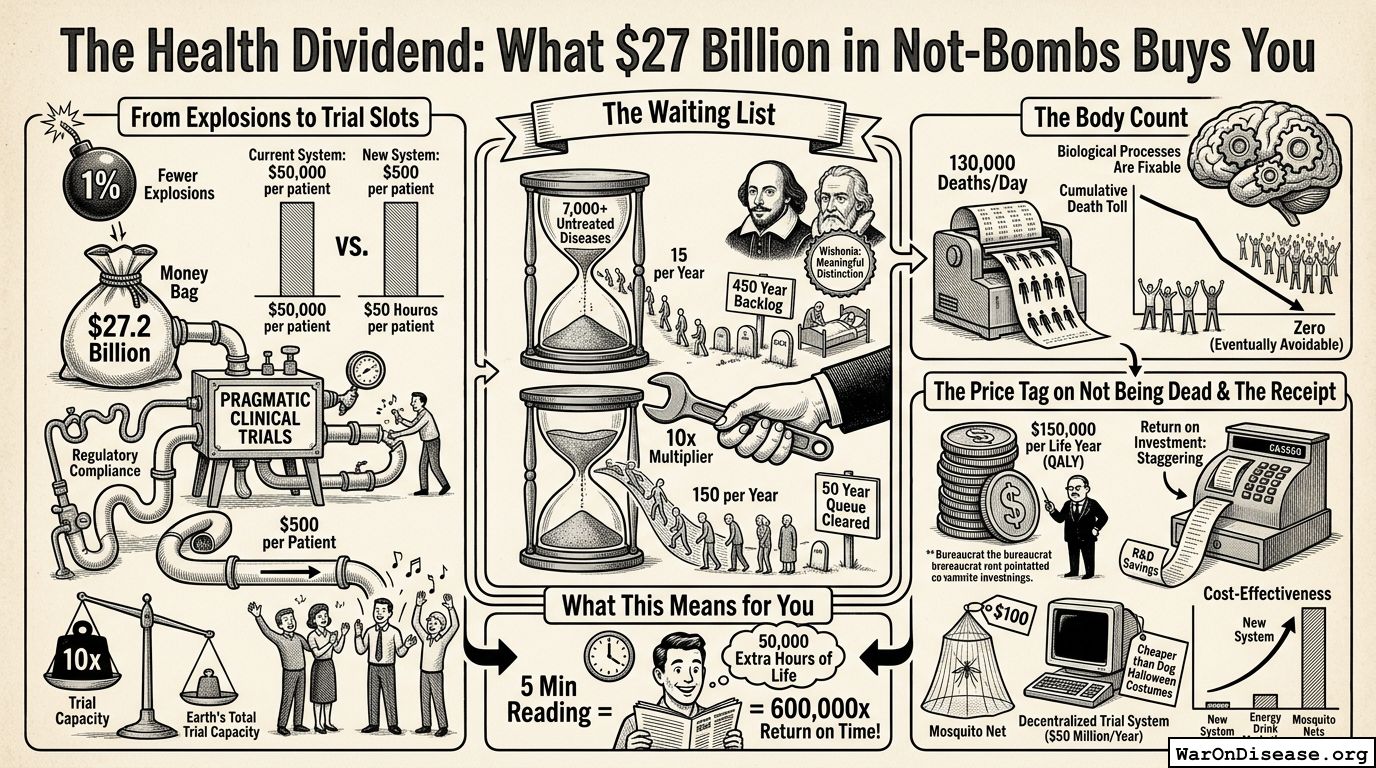

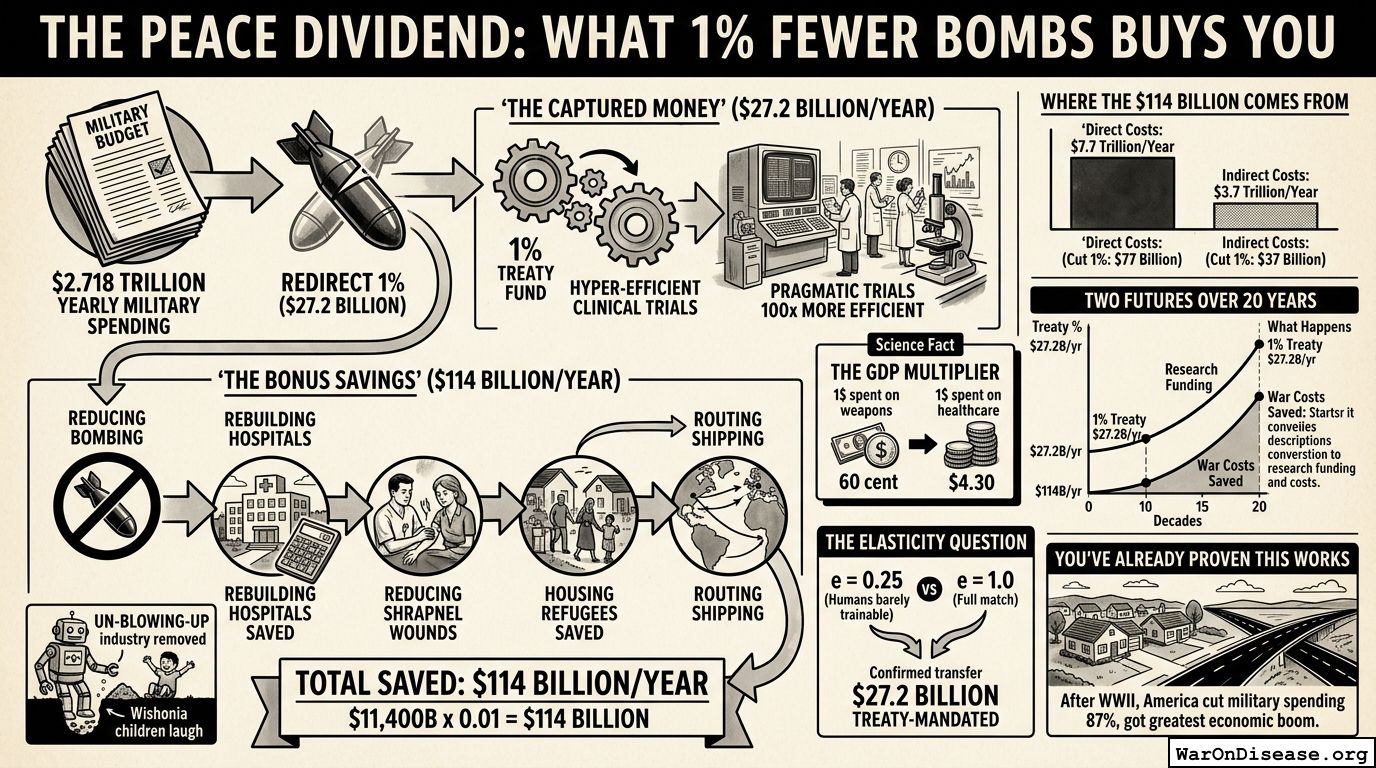

Move 1% of the $2.7T bomb budget to medicine: $27.2B for trials, $114B saved from fewer explosions. Your worst case is the largest medical funding increase in history.